Attorney-Verified Business Bill of Sale Template

Attorney-Verified Business Bill of Sale Template

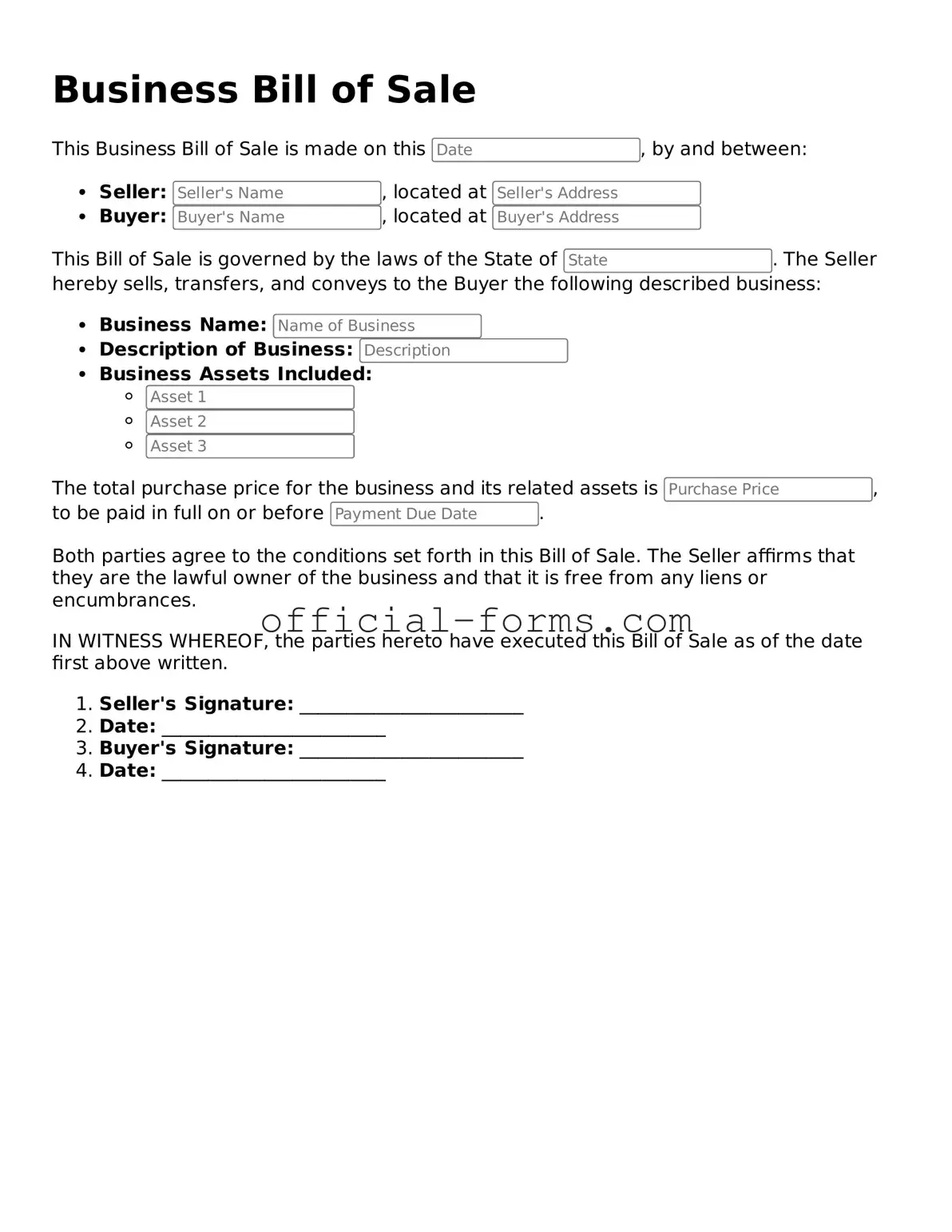

The Business Bill of Sale form serves as a crucial document in the transfer of ownership of a business or its assets. This form typically outlines essential details such as the names and addresses of the buyer and seller, a description of the business or assets being sold, and the sale price. Additionally, it may include terms of the sale, such as any warranties or representations made by the seller regarding the condition of the business or assets. Properly completing this form helps protect both parties by providing a clear record of the transaction, which can be important for legal and tax purposes. Furthermore, the Business Bill of Sale can serve as evidence of the transfer in case of disputes or future claims. Understanding the components and implications of this form is vital for anyone involved in buying or selling a business, ensuring that the transaction is conducted smoothly and in accordance with applicable laws.

Private Gun Sale Bill of Sale - The form can help establish the buyer's eligibility to own a firearm.

In the state of Wisconsin, ensuring a smooth transfer of ownership when buying or selling a vehicle is essential, and the Wisconsin Motor Vehicle Bill of Sale form plays a vital role in this process. This document not only confirms the transaction details but also serves as a legal record that is important for registration and tax assessment. For more information on how to obtain this form, you can visit autobillofsaleform.com/wisconsin-motor-vehicle-bill-of-sale-form/.

Bill of Sale Template for Boat - Serves as proof of purchase for future reference.

Completing a Business Bill of Sale is an important step in the process of transferring ownership of a business. Once you have gathered the necessary information, you can proceed with filling out the form accurately to ensure a smooth transaction.

After completing the form, ensure that both parties retain a copy for their records. This document serves as proof of the transaction and can be essential for future reference.

When filling out and using the Business Bill of Sale form, consider the following key takeaways:

Filling out a Business Bill of Sale form can be straightforward, but many individuals make common mistakes that can lead to complications later. One frequent error is failing to include all necessary details about the business being sold. This includes the name, address, and any relevant identification numbers. Omitting this information can create confusion and may lead to disputes down the line.

Another mistake is not accurately listing the items or assets included in the sale. Buyers need a clear understanding of what they are acquiring. If specific equipment, inventory, or intellectual property is not detailed, it can result in misunderstandings or unmet expectations.

Many people also overlook the importance of including the sale price. Leaving this blank or stating an incorrect amount can create legal issues. Both parties need to agree on the price to ensure a smooth transaction and to avoid potential disputes in the future.

Additionally, failing to include signatures from both the seller and buyer is a critical error. A Business Bill of Sale is not legally binding without these signatures. Ensure that both parties sign and date the document to validate the transaction.

Some individuals may rush through the form, neglecting to read the terms and conditions carefully. This can lead to misunderstandings about warranties or liabilities. It is essential to understand what is being agreed upon to avoid future complications.

Finally, not keeping a copy of the completed Bill of Sale can be detrimental. Both parties should retain a copy for their records. This document serves as proof of the transaction and can be crucial if any issues arise later.

When completing a business transaction, particularly the sale of a business, several important documents accompany the Business Bill of Sale. Each of these forms serves a specific purpose and helps ensure that the transaction is clear, legal, and binding. Below is a list of commonly used documents in conjunction with a Business Bill of Sale.

Each of these documents plays a vital role in facilitating a smooth transaction. By understanding their purpose, both buyers and sellers can navigate the process with greater confidence and clarity.