Official California Loan Agreement Document

Official California Loan Agreement Document

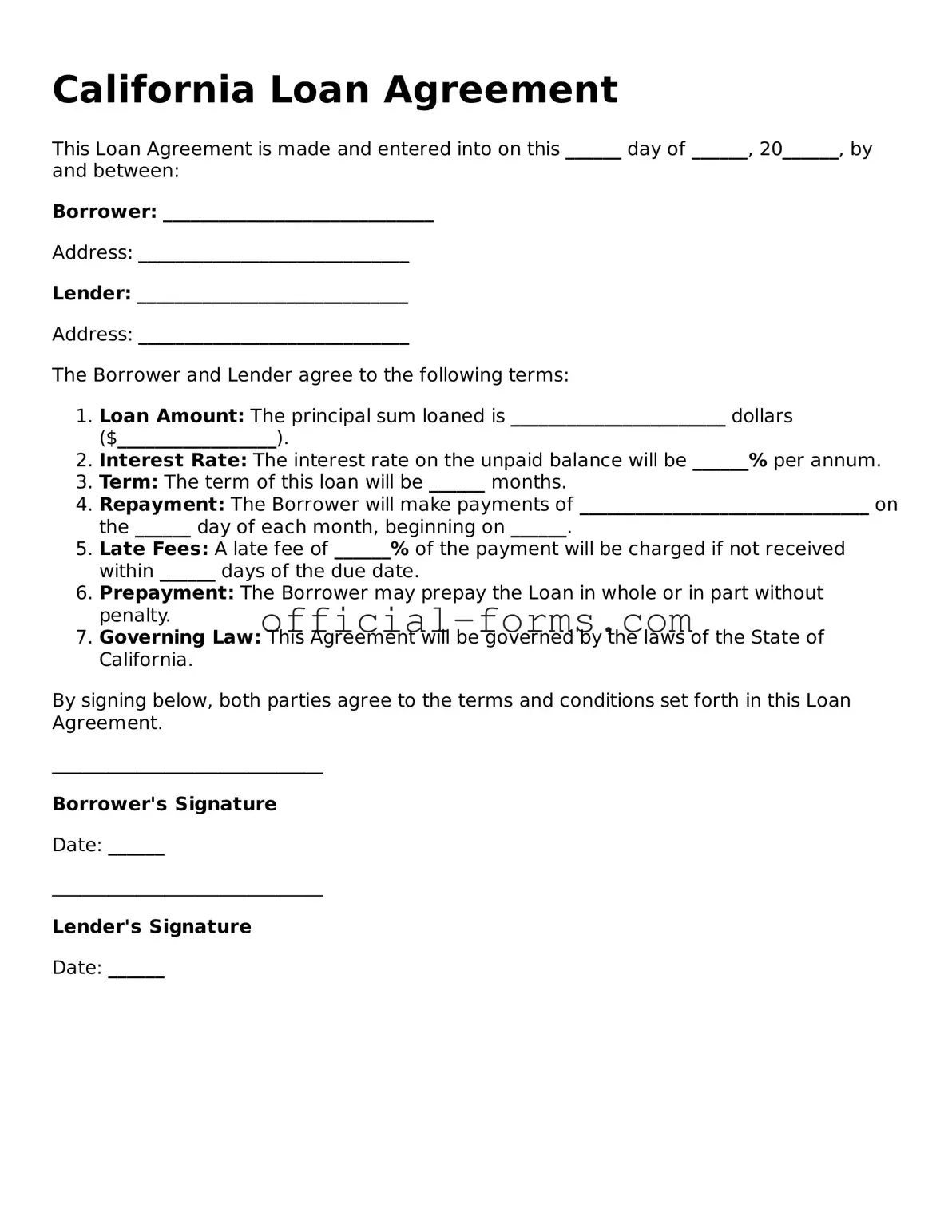

The California Loan Agreement form serves as a vital document in the realm of personal and business finance, providing a structured approach to borrowing and lending money. This form outlines the terms and conditions under which a borrower receives funds from a lender, ensuring that both parties have a clear understanding of their rights and obligations. Key aspects of the agreement include the loan amount, interest rate, repayment schedule, and any collateral that may secure the loan. Additionally, it addresses potential penalties for late payments and the process for resolving disputes. By detailing these elements, the Loan Agreement form helps to protect the interests of both the lender and the borrower, fostering transparency and accountability in financial transactions. Understanding this form is essential for anyone involved in a loan process in California, whether for personal use, real estate, or business purposes.

Loan Agreement Template Texas - Borrowers should fully understand the Loan Agreement before signing.

Promissory Note Template Illinois - Loan Agreements can be customized based on the needs of the parties involved.

Promissory Note Template New York - A Loan Agreement outlines the terms between a borrower and a lender.

When engaging in a vehicle sale in Virginia, it's important to utilize the correct paperwork to safeguard both parties involved in the transaction. The Virginia Motor Vehicle Bill of Sale form is essential for this purpose, providing clarity and legality to the transfer process. For more information on obtaining and completing this form, you can visit https://autobillofsaleform.com/virginia-motor-vehicle-bill-of-sale-form/, ensuring a hassle-free experience.

Promissory Note Template Wisconsin - The form affirms the mutual understanding of the financial arrangement.

Once you have the California Loan Agreement form in front of you, it's time to start filling it out. This process involves providing specific information that outlines the terms of the loan, ensuring both parties are clear on their responsibilities. Follow these steps carefully to complete the form accurately.

After completing the form, review it carefully for any errors or missing information. Ensuring accuracy will help prevent misunderstandings later on. Once everything is in order, both parties can keep a copy for their records.

When it comes to filling out and using the California Loan Agreement form, there are several important points to keep in mind. Understanding these key takeaways can help ensure that the process goes smoothly and that both parties are protected.

By keeping these takeaways in mind, you can navigate the loan agreement process with confidence, ensuring that both lenders and borrowers understand their rights and responsibilities.

Filling out the California Loan Agreement form can be a straightforward process, but many individuals make common mistakes that can lead to complications. One frequent error is failing to provide complete personal information. Borrowers often overlook details such as their full legal name, current address, or Social Security number. Incomplete information can delay processing and may even result in the rejection of the application.

Another mistake involves not clearly stating the loan amount. Borrowers sometimes write ambiguous figures or fail to specify whether the amount is in dollars or another currency. Clarity is essential to avoid misunderstandings later on. Always ensure that the loan amount is clearly indicated and formatted correctly.

Additionally, many people neglect to review the interest rate section. Some borrowers either do not understand how to calculate the interest or simply leave it blank. This can lead to disputes over repayment terms. It’s crucial to double-check this section and ensure that it reflects the agreed-upon rate.

Another common error is skipping the repayment terms. Borrowers often forget to specify how and when payments will be made. This oversight can create confusion and lead to missed payments. Clearly outlining the repayment schedule helps both parties understand their obligations.

People also frequently ignore the need for signatures. Some may assume that a verbal agreement is sufficient, but a signed document is essential for legal enforceability. Ensure that all parties involved sign the agreement to validate the terms.

Inadequate documentation is another significant mistake. Borrowers sometimes fail to attach necessary supporting documents, such as proof of income or credit history. These documents are vital for the lender to assess risk and make informed decisions.

Misunderstanding or misrepresenting the purpose of the loan can also lead to issues. Borrowers should clearly articulate why they are seeking the loan. Misrepresentation can not only jeopardize the loan approval but may also have legal ramifications.

People often overlook the importance of understanding the terms and conditions of the loan. Failing to read the fine print can lead to unexpected fees or penalties. Taking the time to thoroughly review the agreement can prevent future disputes.

Finally, some borrowers forget to keep a copy of the signed agreement. This document serves as a critical reference point for both parties. Without it, resolving any issues that arise later can become challenging. Always ensure that a copy is retained for personal records.

When entering into a loan agreement in California, several other documents may accompany the main loan agreement to ensure clarity and protection for both parties involved. Here’s a brief overview of some common forms and documents you might encounter.

These documents work together to create a comprehensive understanding of the loan arrangement, protecting both the lender and the borrower. Having them in place helps facilitate a smooth transaction and reduces the risk of misunderstandings down the line.