Official Florida Promissory Note Document

Official Florida Promissory Note Document

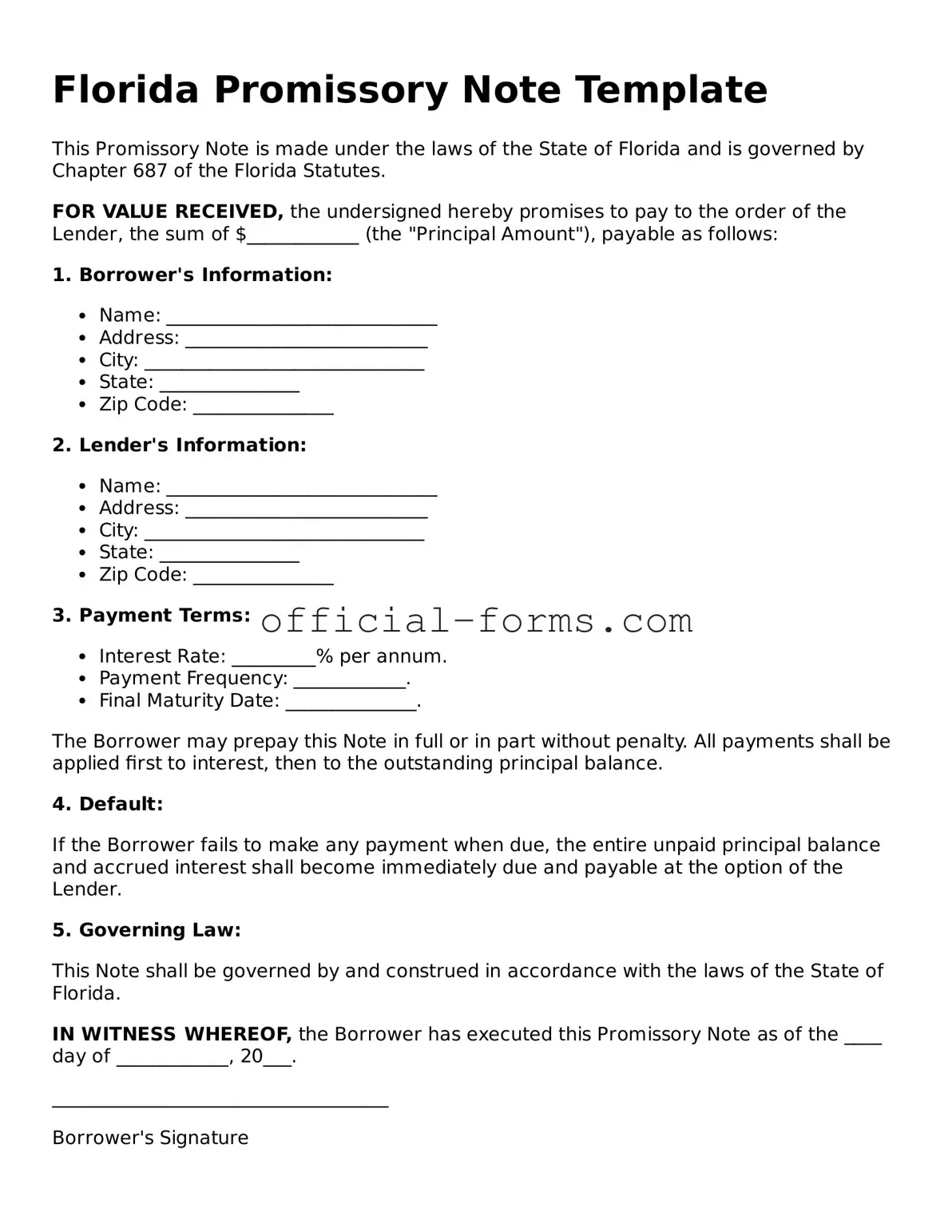

The Florida Promissory Note form is an essential financial document used in lending transactions within the state. It outlines the borrower's promise to repay a specified amount of money to the lender under agreed-upon terms. Key components of this form include the principal amount, interest rate, repayment schedule, and maturity date. Additionally, it may address late fees, prepayment options, and the consequences of default. This document serves not only as a record of the loan agreement but also as a legal tool that can be enforced in court if necessary. Understanding the intricacies of the Florida Promissory Note is crucial for both borrowers and lenders to ensure a clear and binding agreement that protects their respective interests.

Ohio Promissory Note Requirements - The Promissory Note may also permit early repayment without penalties.

Having a properly executed Arizona ATV Bill of Sale form is essential for both buyers and sellers, as it solidifies the ownership transfer and provides legal protection for both parties. For those looking to simplify this process, you can access a customizable template at billofsaleforvehicles.com/editable-arizona-atv-bill-of-sale, ensuring that all necessary details are accurately captured and the transaction is documented correctly.

Rhode Island Standard Promissory Note - When creating a promissory note, specificity in terms can help prevent misunderstandings.

Once you have the Florida Promissory Note form ready, you will need to fill it out carefully to ensure all necessary information is included. This document outlines the terms of a loan agreement between a borrower and a lender. Follow these steps to complete the form correctly.

Once you have completed the form, make sure to keep a copy for your records. It’s also a good idea to review the document with both parties before finalizing it to ensure everyone is on the same page.

Filling out a Florida Promissory Note form can seem straightforward, but many individuals make common mistakes that can lead to complications later on. Understanding these pitfalls is essential for ensuring that the document is valid and enforceable.

One frequent mistake is failing to include all necessary information. A Promissory Note must clearly state the names of the borrower and lender, the loan amount, interest rate, and repayment terms. Omitting any of these details can render the note incomplete and potentially unenforceable.

Another common error involves incorrect dates. It is crucial to specify the date the note is signed and the date when payments are due. If these dates are left blank or inaccurately filled in, it may create confusion regarding the terms of the loan.

Some individuals also neglect to clarify the payment schedule. Whether payments are to be made monthly, quarterly, or on another schedule, this must be clearly outlined in the note. Vague language can lead to misunderstandings and disputes between the parties involved.

Additionally, many people forget to include a default clause. This clause outlines what happens if the borrower fails to make payments as agreed. Without this provision, the lender may have limited options for recourse in the event of default.

Finally, not having the document properly signed can be a significant oversight. Both parties must sign the Promissory Note for it to be legally binding. Additionally, having a witness or notarization can further strengthen the enforceability of the document.

By avoiding these common mistakes, individuals can ensure that their Florida Promissory Note serves its intended purpose and protects their interests effectively.

When entering into a financial agreement, particularly one involving a promissory note in Florida, several additional documents may be necessary to ensure clarity and legal protection for all parties involved. Below is a list of commonly used forms that accompany a Florida Promissory Note.

Each of these documents plays a crucial role in the loan process, providing structure and protection for both lenders and borrowers. Properly preparing and understanding these forms can help avoid misunderstandings and legal complications down the line.