Official Georgia Promissory Note Document

Official Georgia Promissory Note Document

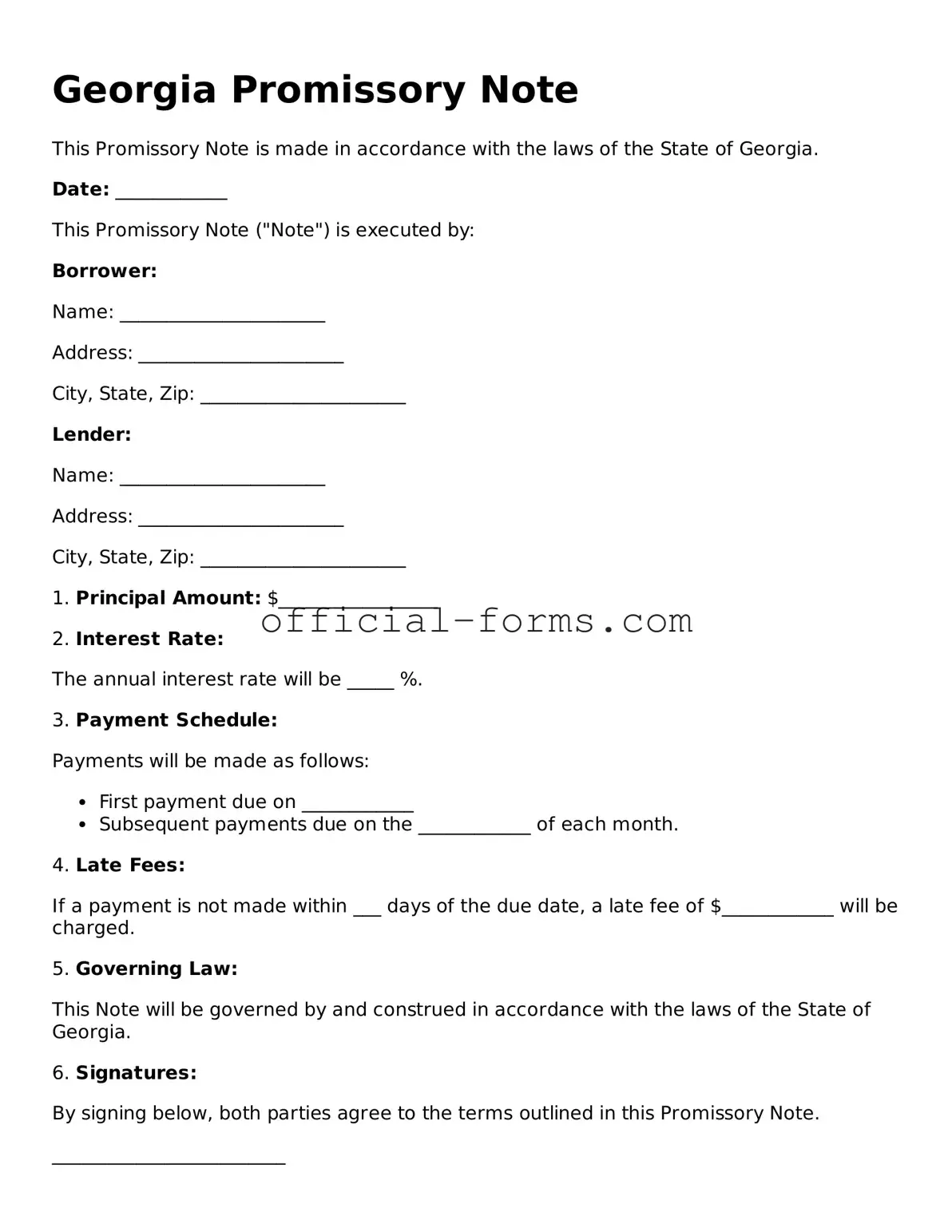

In the realm of financial transactions, the Georgia Promissory Note serves as a crucial instrument for establishing a clear agreement between a borrower and a lender. This legally binding document outlines the terms under which a borrower promises to repay a specified sum of money to the lender, often including details such as the interest rate, repayment schedule, and any applicable late fees. It is essential for both parties to understand their rights and obligations as stipulated within the note, ensuring that the terms are transparent and enforceable. The form typically requires essential information such as the names and addresses of the parties involved, the principal amount borrowed, and the date of execution. Additionally, it may include provisions for default, outlining the consequences should the borrower fail to meet their obligations. By utilizing the Georgia Promissory Note, individuals and businesses can facilitate loans with confidence, knowing that they have a documented agreement that can protect their interests in the event of a dispute.

Kansas Promissory Note - Defaulting on a promissory note can lead to legal consequences for the borrower.

The Georgia Trailer Bill of Sale form is a legal document used to record the transaction details when buying or selling a trailer in the state of Georgia. It serves as proof of purchase and verifies the change of ownership. This form is essential for the buyer's registration and titling process of the trailer, and you can find more information at autobillofsaleform.com/trailer-bill-of-sale-form/georgia-trailer-bill-of-sale-form/.

How to Write a Promissory Note for a Personal Loan - Promissory notes can also outline the consequences of default, including the right to legal remedies.

After obtaining the Georgia Promissory Note form, you'll need to complete it accurately to ensure it serves its intended purpose. Follow these steps carefully to fill out the form correctly.

Once you have filled out the form, review it carefully for any errors. It’s important that all information is accurate and complete before moving forward. After reviewing, keep copies for your records and provide a signed copy to the other party involved in the agreement.

When dealing with a Georgia Promissory Note, it’s important to understand the key aspects to ensure that the document serves its purpose effectively. Here are some essential takeaways:

Understanding these elements will help ensure that the Promissory Note is comprehensive and legally enforceable.

Filling out the Georgia Promissory Note form can seem straightforward, but many people make common mistakes that can lead to complications later. One frequent error is failing to include all necessary information. Each section of the form is important, and missing details can render the note invalid.

Another mistake is not clearly stating the loan amount. This figure should be precise. Ambiguities can lead to disputes over how much is actually owed. It's essential to write the amount both in numbers and words to avoid any confusion.

People often overlook the interest rate. If the interest rate is not specified, the note may be considered a gift rather than a loan. Ensure that the interest rate complies with Georgia's usury laws to avoid legal issues.

Additionally, signatories sometimes forget to date the document. A date is crucial as it marks the beginning of the loan period. Without it, there could be questions about when repayment is due.

Another common error involves not having witnesses or a notary. While not always required, having these can provide additional legal protection. It helps to verify that the signatures are legitimate and that both parties understood the terms.

People may also neglect to read the entire document before signing. Understanding every term is vital. Misinterpretations can lead to unexpected obligations or rights.

Lastly, failing to keep a copy of the signed note is a significant oversight. Both parties should retain a copy for their records. This ensures that everyone is on the same page regarding the terms of the agreement.

When dealing with a Georgia Promissory Note, several other forms and documents may be necessary to ensure a smooth transaction. Understanding these documents can help you navigate the lending process more effectively. Here’s a list of important forms often used alongside a Promissory Note:

Having these documents in place can protect both the lender and the borrower. It’s essential to understand each document's purpose and ensure that they are completed accurately. This will help facilitate a clear and legally sound lending process.