Official Illinois Promissory Note Document

Official Illinois Promissory Note Document

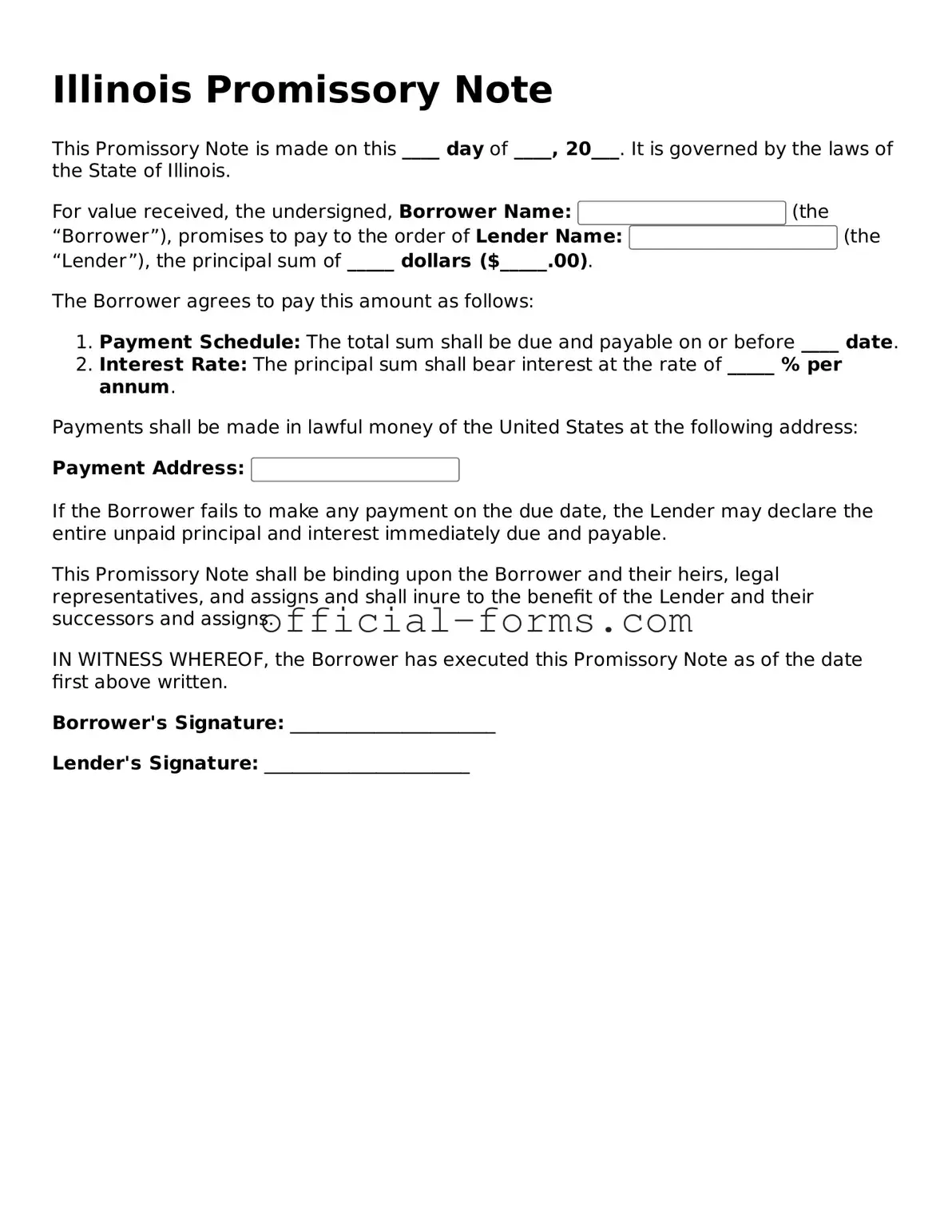

In the realm of financial transactions, the Illinois Promissory Note serves as a crucial instrument for documenting a borrower's promise to repay a specific amount of money to a lender under agreed-upon terms. This form outlines essential elements such as the principal amount, interest rate, repayment schedule, and any applicable fees, ensuring clarity and mutual understanding between the parties involved. Importantly, the note may also specify the consequences of default, detailing the actions that may be taken should the borrower fail to meet their obligations. By providing a structured format for these agreements, the Illinois Promissory Note not only facilitates secure lending practices but also enhances the enforceability of the terms, thereby protecting the interests of both lenders and borrowers. Understanding the intricacies of this document is vital for anyone engaging in lending or borrowing activities, as it lays the foundation for a transparent financial relationship.

How to Write a Promissory Note for a Personal Loan - The repayment terms should be realistic and adhere to both parties' financial capabilities.

Additionally, for those involved in the buying or selling of trailers, accessing the necessary paperwork is essential. The California Trailer Bill of Sale form not only facilitates the transfer of ownership but also acts as a protective measure for both the seller and the buyer. To ensure you have the right documentation, consider visiting autobillofsaleform.com/trailer-bill-of-sale-form/california-trailer-bill-of-sale-form for a comprehensive guide on obtaining this vital form.

How to Write a Promissory Note - The borrower can use a promissory note for large or small amounts of money.

Sample Promissory Note California - The document includes essential details such as the names of the parties involved.

After you have gathered all necessary information, it’s time to fill out the Illinois Promissory Note form. Completing this form accurately is essential for ensuring that all parties involved understand their obligations. Follow these steps carefully to ensure that the form is filled out correctly.

Once you have completed the form, review it thoroughly to ensure all information is accurate and complete. Make copies for both the borrower and lender, and store the original in a safe place. This step is crucial for maintaining a record of the agreement.

When it comes to filling out and using the Illinois Promissory Note form, understanding the essentials can make the process smoother. Here are some key takeaways to consider:

By following these guidelines, both borrowers and lenders can ensure that the promissory note is filled out correctly and serves its intended purpose.

Filling out the Illinois Promissory Note form requires careful attention to detail. One common mistake is failing to include all necessary information. The form requires specific details such as the names of the borrower and lender, the amount borrowed, and the repayment terms. Omitting any of this information can lead to confusion or disputes later on.

Another frequent error is not clearly stating the interest rate. If an interest rate is applicable, it should be clearly defined. Vague language or missing information about the interest can create misunderstandings about the total amount to be repaid.

Some individuals overlook the importance of signatures. Both the borrower and lender must sign the document for it to be legally binding. Failing to obtain the necessary signatures renders the note ineffective, which can complicate any future collection efforts.

Inaccurate dates are also a common issue. It is crucial to ensure that the date of the agreement is correct. An incorrect date can affect the enforceability of the note and may lead to complications in tracking repayment timelines.

Another mistake involves not specifying the repayment schedule. Whether payments are to be made monthly, quarterly, or in a lump sum, this should be clearly outlined. Without a defined schedule, it may be difficult to determine when payments are due.

People sometimes neglect to include provisions for default. It is advisable to outline what happens if the borrower fails to make a payment. This can include late fees or legal actions, and having these terms in writing can help protect the lender’s interests.

Finally, individuals may not keep copies of the completed Promissory Note. Both parties should retain a signed copy for their records. This ensures that both the borrower and lender have access to the same information, which can be essential in case of disputes.

When entering into a loan agreement, the Illinois Promissory Note is a key document. However, several other forms and documents often accompany it to ensure clarity and legal protection for both parties involved. Below is a list of these documents, each serving a specific purpose in the transaction.

Each of these documents plays a vital role in the lending process. They help protect both the lender's and borrower's interests, ensuring a clear understanding of the loan agreement and its implications. Properly managing these documents can lead to a smoother transaction and minimize potential disputes.