Blank IRS 941 Form

Blank IRS 941 Form

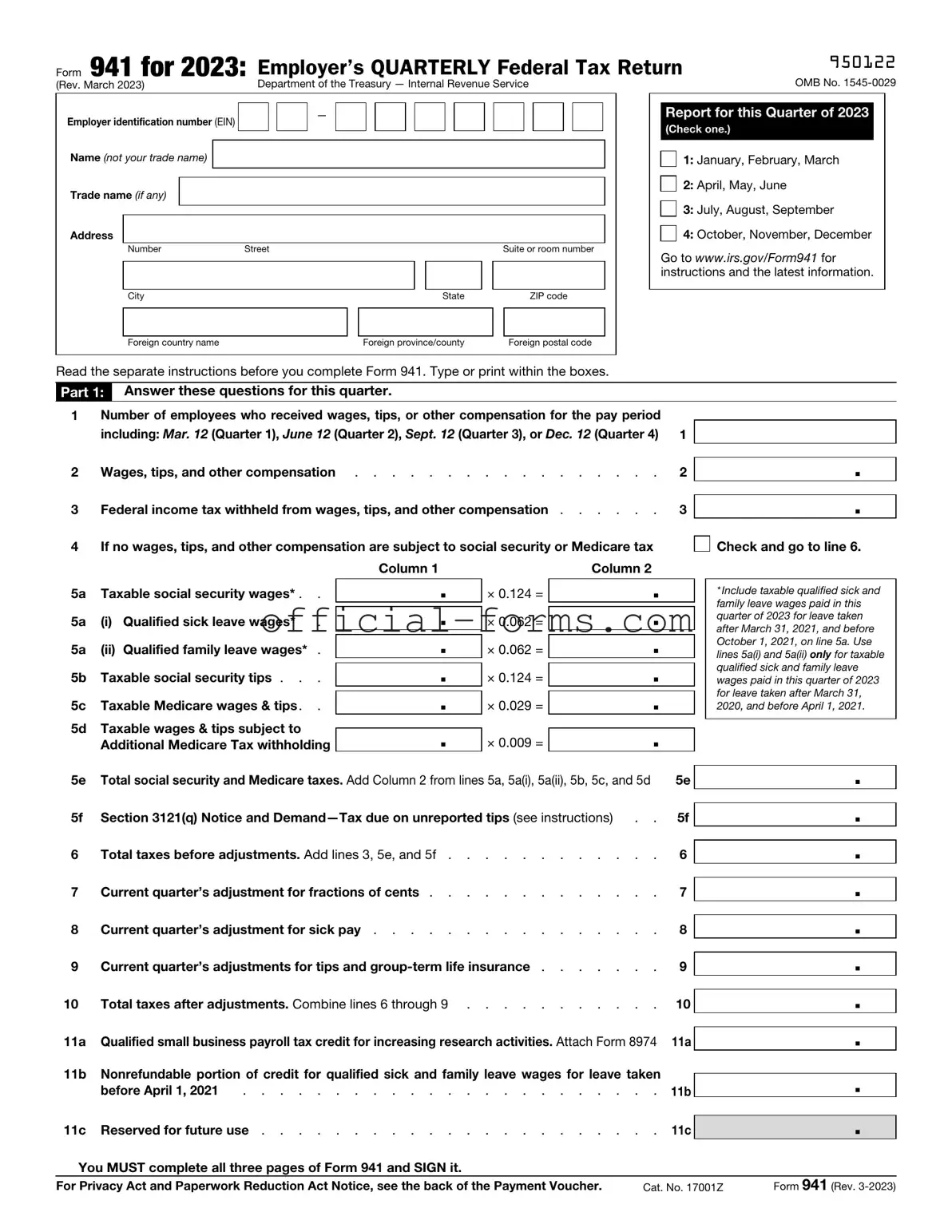

The IRS Form 941 plays a crucial role in the realm of payroll taxes for employers across the United States. This quarterly tax return is designed for businesses to report income taxes, Social Security tax, and Medicare tax withheld from employees' paychecks. Employers use this form to reconcile the amounts withheld with the taxes they owe, ensuring compliance with federal regulations. Each quarter, businesses must accurately calculate and report the total wages paid, the number of employees, and the amounts withheld for federal income tax, Social Security, and Medicare. Additionally, Form 941 allows employers to claim any adjustments for overpayments or errors from previous quarters. Timely filing of this form is essential, as it helps avoid penalties and interest charges that can arise from late submissions or inaccuracies. Understanding the nuances of Form 941 can significantly impact a business's financial health and compliance standing.

Fedex Reprint Label - Weight and dimensions must be recorded accurately for freight assessment.

To facilitate a smooth transaction, it is advisable to use the Arizona ATV Bill of Sale form available through AZ Forms Online, which aids in capturing all necessary details for the sale and transfer of ownership, ensuring that both the buyer and seller maintain a clear and legally recognized record of the sale.

Job Application in Spanish - Be aware of deadlines for submitting the application if applicable.

Da Form 31 - The approval process involves several levels of authority signatures, each needing to be recorded.

Filling out the IRS Form 941 is essential for employers to report payroll taxes. This form must be submitted quarterly. Follow these steps to ensure accurate completion.

After submission, retain a copy of the completed form for your records. It is important to keep track of any correspondence from the IRS regarding your submission.

Filling out and using the IRS Form 941 is crucial for employers in the United States. This form is used to report income taxes, Social Security tax, and Medicare tax withheld from employee paychecks. Here are key takeaways to keep in mind:

Understanding these key points can help ensure compliance with IRS requirements and avoid potential penalties.

Filling out the IRS Form 941 can be a straightforward process, but many people make common mistakes that can lead to delays or penalties. One frequent error is failing to report all wages accurately. Employers must include all taxable wages, tips, and other compensation. Omitting even a small amount can result in discrepancies that raise red flags with the IRS.

Another mistake involves miscalculating the tax liability. Some individuals misinterpret the instructions or misapply the tax rates. This can lead to underreporting or overreporting the amount owed, which can trigger audits or additional penalties. Always double-check calculations to ensure accuracy.

Many people also neglect to sign and date the form. A missing signature can delay processing and cause the IRS to consider the form incomplete. This simple oversight can lead to significant complications, including late fees or additional scrutiny.

Incorrectly identifying the employer's identification number (EIN) is another common issue. The EIN must be accurate and match the IRS records. Errors in this number can result in confusion and processing delays, as the IRS may not be able to link the form to the correct employer.

Some filers forget to account for adjustments. If there were any corrections or adjustments from previous quarters, these need to be reflected on the current Form 941. Failing to include these adjustments can lead to inaccurate reporting and potential penalties.

Additionally, individuals often make mistakes regarding the quarter being reported. Each form corresponds to a specific quarter, and submitting a form for the wrong quarter can lead to unnecessary complications. Always verify the quarter before submission.

Another mistake involves misunderstanding the deadlines. The IRS has specific due dates for Form 941, and late submissions can incur penalties. It's crucial to stay informed about these deadlines to avoid unnecessary fees.

Some employers mistakenly believe they can file Form 941 annually instead of quarterly. This misconception can lead to significant compliance issues. Form 941 must be filed quarterly, and failing to do so can result in penalties.

Finally, neglecting to keep copies of submitted forms can be a costly mistake. Employers should retain copies for their records, as they may need to reference them in the future. Keeping thorough records helps ensure compliance and simplifies the process in case of an audit.

The IRS Form 941 is essential for employers to report income taxes, Social Security tax, and Medicare tax withheld from employee paychecks. However, several other forms and documents often accompany it to ensure compliance with tax obligations. Below are four important documents that may be used alongside Form 941.

Understanding these forms and their purposes can help ensure that employers remain compliant with federal tax regulations. Keeping accurate records and timely filing will protect against penalties and ensure smooth operations for your business.