Attorney-Verified Loan Agreement Template

Attorney-Verified Loan Agreement Template

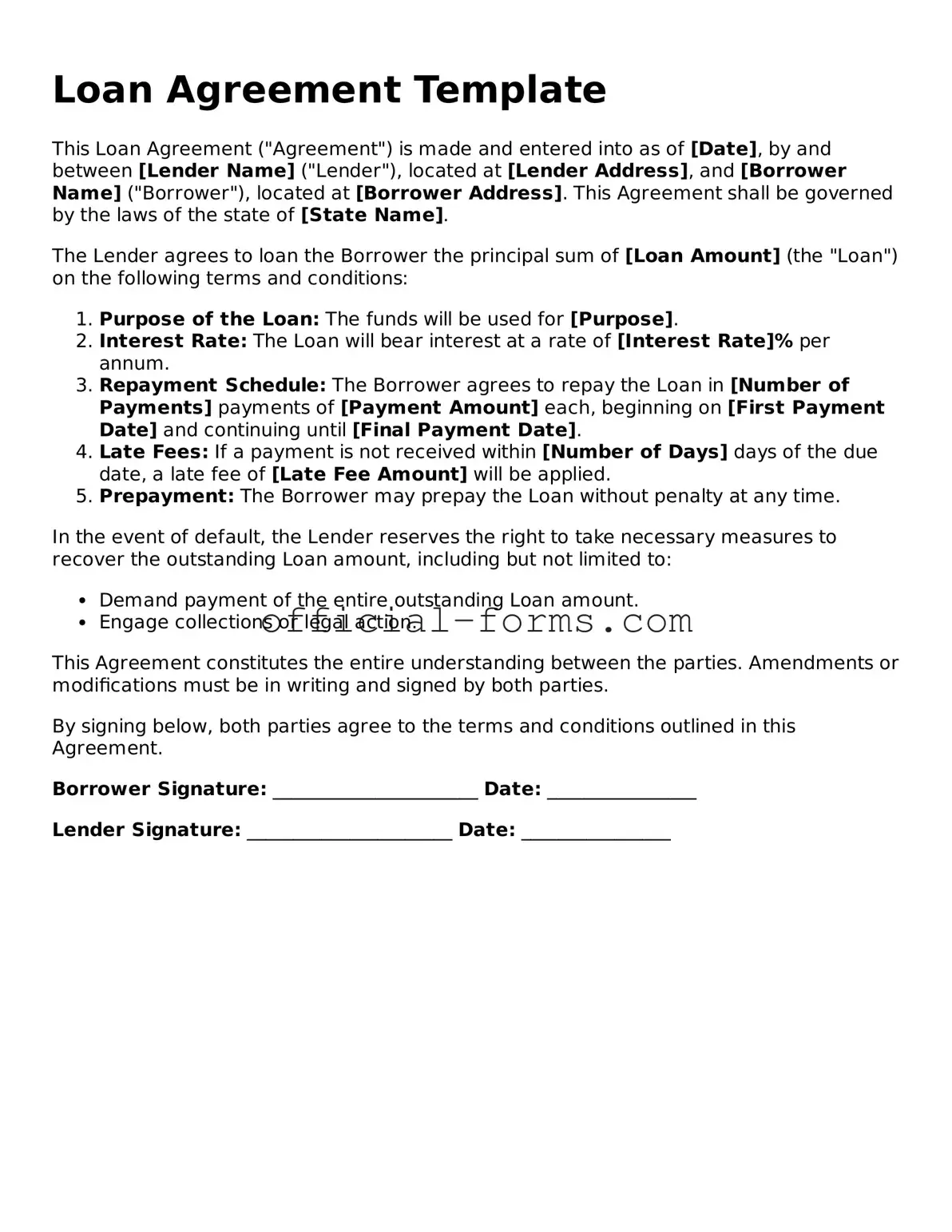

When entering into a loan agreement, understanding the essential components of the form is crucial for both borrowers and lenders. This document serves as a binding contract that outlines the terms and conditions of the loan, ensuring clarity and protection for all parties involved. Key aspects include the loan amount, interest rate, repayment schedule, and any applicable fees. Additionally, the agreement specifies the consequences of default, the rights of both the borrower and lender, and any collateral involved in securing the loan. By clearly defining these elements, the loan agreement helps prevent misunderstandings and disputes, fostering a transparent relationship between the parties. Whether you are borrowing money for personal reasons or seeking funding for a business venture, familiarizing yourself with this form is an important step in the borrowing process.

Personnel Change Form - Accurately reflect changes in workplace policies affecting employees.

In addition to completing the California LLC-1 form, entrepreneurs can find further resources and support by visiting California Documents Online, which offers guidance on the necessary steps for forming a Limited Liability Company in California.

Commercial Lease Proposal - The letter also allows landlords to present any additional fees or expenses that may be associated with the lease.

Completing the Loan Agreement form is essential for establishing the terms of the loan. Follow the steps below to ensure accurate and complete information is provided.

When filling out and using a Loan Agreement form, several important points should be kept in mind. Here are four key takeaways:

Filling out a Loan Agreement form can be a straightforward process, but mistakes can lead to complications. One common error is providing inaccurate personal information. Borrowers may overlook details such as their full legal name, address, or Social Security number. This can result in delays or even denial of the loan.

Another frequent mistake is failing to read the terms and conditions carefully. Many individuals rush through the form without understanding the implications of the agreement. This can lead to unexpected fees or obligations that were not anticipated at the time of signing.

People often forget to include necessary documentation. Lenders typically require proof of income, employment verification, and identification. Omitting these documents can slow down the approval process or cause the application to be rejected.

In addition, some borrowers may not disclose all outstanding debts. Lenders assess a borrower's ability to repay based on their total financial picture. Failing to report existing loans or credit card debt can lead to a miscalculation of the borrower's financial capacity.

Another mistake involves misunderstanding interest rates. Borrowers may confuse fixed and variable rates or fail to recognize how interest will accumulate over time. This misunderstanding can result in financial strain if payments are higher than expected.

Moreover, people sometimes overlook the importance of a co-signer. If the borrower has a limited credit history or poor credit score, a co-signer can strengthen the application. Neglecting to consider this option may reduce the chances of loan approval.

Some individuals also fail to ask questions about the loan process. It is essential to clarify any uncertainties regarding repayment terms, penalties for late payments, or the consequences of defaulting. Not seeking this information can lead to misunderstandings later on.

Lastly, a significant error is not keeping copies of the completed Loan Agreement form. Having a record of the signed document is crucial for future reference. Without it, borrowers may find themselves in disputes or unable to track their obligations.

When entering into a loan agreement, several additional forms and documents may be necessary to ensure clarity and legal compliance. These documents help outline the terms of the loan and protect the interests of both the lender and the borrower. Below is a list of commonly used documents that accompany a loan agreement.

These documents play a crucial role in the lending process. By understanding their purpose, borrowers can navigate their financial obligations more effectively and lenders can mitigate risks associated with lending. It is always advisable to review each document carefully before signing.