Blank Mortgage Statement Form

Blank Mortgage Statement Form

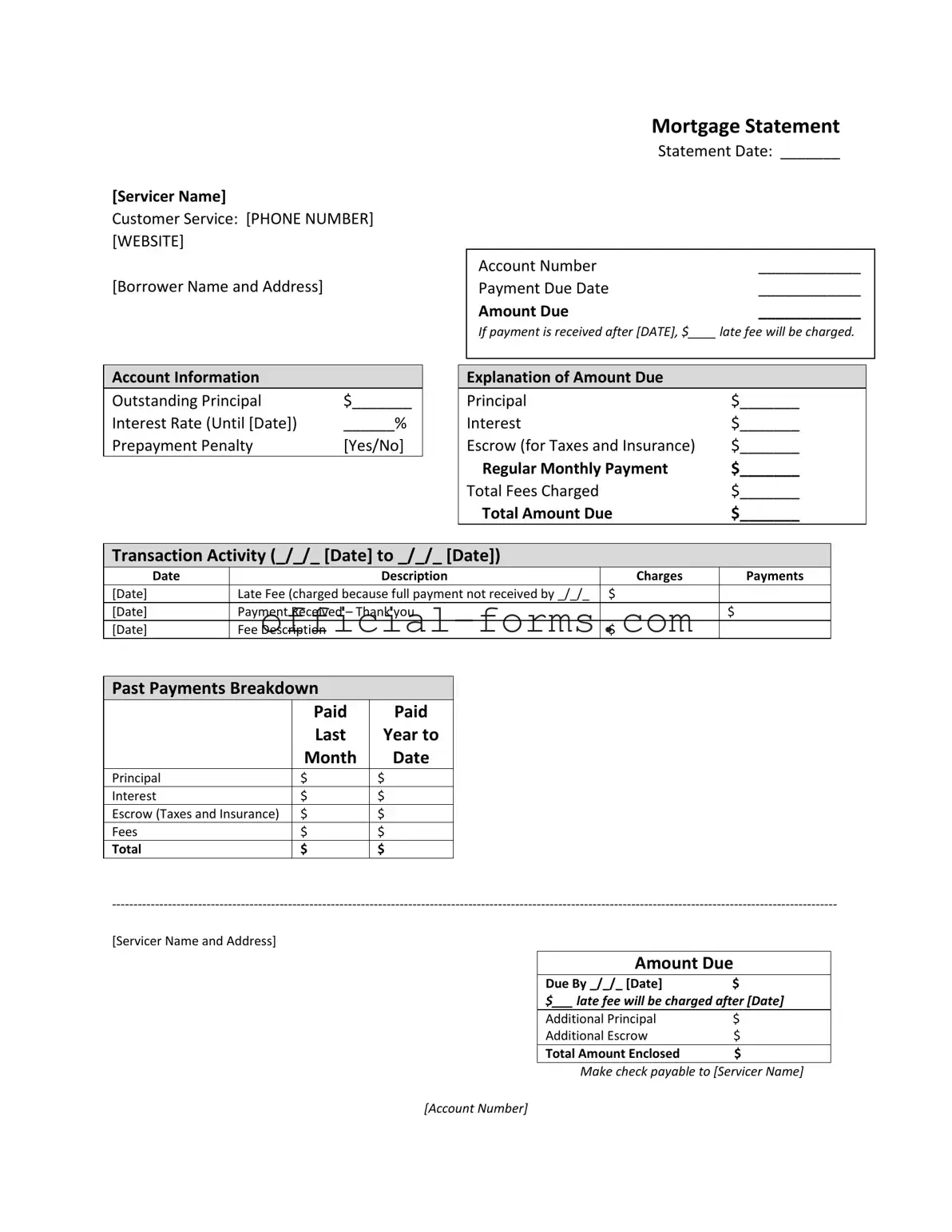

The Mortgage Statement form serves as a crucial document for homeowners, providing a detailed overview of their mortgage account. It includes essential information such as the servicer's name, customer service contact details, and the borrower's name and address. Key dates, including the statement date, payment due date, and account number, are prominently displayed. The form outlines the amount due and specifies any late fees that may apply if payment is not received on time. Account information is clearly detailed, showing the outstanding principal, interest rate, and whether a prepayment penalty applies. A breakdown of the amount due is provided, including principal, interest, escrow for taxes and insurance, and total fees charged. Transaction activity is listed to give borrowers insight into their payment history, including any late fees incurred and payments received. Additionally, the form contains important messages regarding partial payments and delinquency notices, alerting borrowers to the consequences of late payments. For those facing financial difficulties, the statement directs them to resources for mortgage counseling or assistance, ensuring that help is available when needed.

Business Bureau - I experienced a billing error, which caused financial difficulties.

For those needing to address inaccuracies in official records, understanding the importance of the Affidavit of Correction process is crucial. You can find more information about the vital steps involved in the effective completion of the necessary Affidavit of Correction documentation.

Dd Form 2656 March 2022 - Members of the armed forces file this form to initiate their retired pay process.

Filling out the Mortgage Statement form requires careful attention to detail. This form is essential for managing your mortgage account. Follow these steps to ensure accurate completion.

Understanding the Mortgage Statement form is crucial for homeowners. Here are key takeaways to help you navigate this important document:

By keeping these points in mind, you can effectively manage your mortgage and ensure you stay on top of your payments. Always refer to the statement for the most accurate information regarding your mortgage account.

Filling out the Mortgage Statement form can be straightforward, but mistakes can lead to confusion and delays. One common mistake is not providing the correct account number. This number is crucial for the servicer to identify the right account. Double-checking this information can save time and avoid potential issues.

Another frequent error is failing to include the payment due date. This date is essential for ensuring that payments are made on time. Without it, the servicer may not process the payment correctly, leading to late fees.

People often overlook the amount due section as well. Entering the wrong figure can result in underpayment or overpayment. It is important to verify this amount against previous statements to ensure accuracy.

Many individuals also neglect to review the transaction activity section. This part outlines any charges or payments made during the specified period. Missing this information can lead to misunderstandings about the account's status.

In addition, not addressing the escrow amount can be problematic. This amount is typically used for taxes and insurance. If it is incorrectly filled out, it can affect the overall payment and lead to unexpected costs later on.

Another mistake is not paying attention to the delinquency notice. Ignoring this warning can have serious consequences, including fees and potential foreclosure. It is crucial to understand the implications of any missed payments.

Lastly, individuals sometimes fail to sign or date the form. This oversight can result in the form being rejected or delayed. Ensuring that all required signatures are present is vital for a smooth processing of the mortgage statement.

When managing a mortgage, several important documents accompany the Mortgage Statement form. Each of these documents serves a specific purpose in the mortgage process. Understanding them can help borrowers stay informed and organized.

Being familiar with these documents can empower borrowers to manage their mortgage more effectively. Staying informed helps ensure that all obligations are met and that any issues can be addressed promptly.