Official New York Loan Agreement Document

Official New York Loan Agreement Document

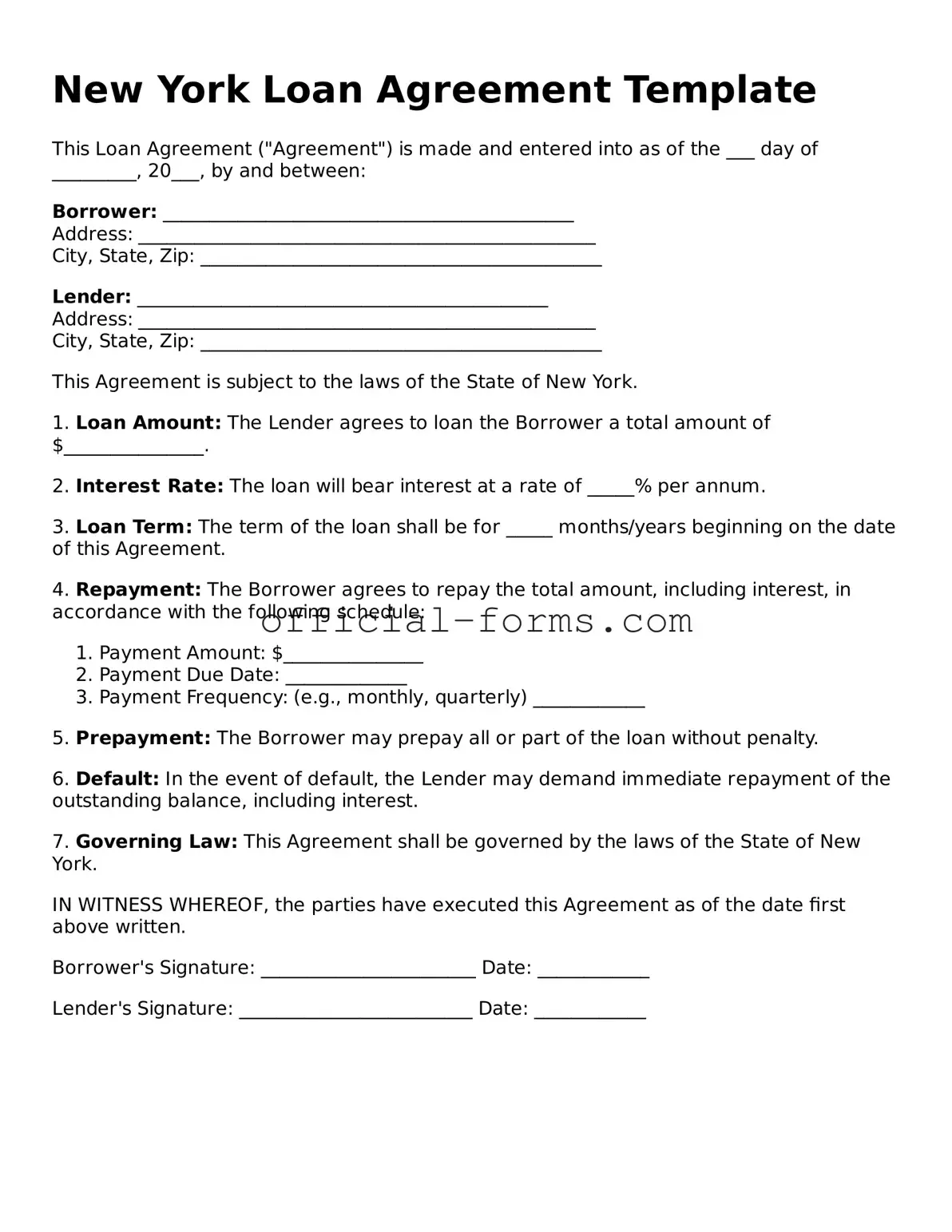

When entering into a financial arrangement in New York, a Loan Agreement form serves as a vital tool for both lenders and borrowers. This document outlines the terms and conditions of the loan, ensuring that all parties understand their rights and obligations. Key components include the loan amount, interest rate, repayment schedule, and any collateral involved. Additionally, it may specify late fees, default terms, and the governing law. By clearly detailing these aspects, the Loan Agreement helps to prevent misunderstandings and disputes down the line. Whether you are borrowing money for personal use or lending it for business purposes, having a well-structured Loan Agreement can provide peace of mind and legal protection for everyone involved.

Loan Note Template - The Loan Agreement should be reviewed carefully to ensure all terms are understood.

Promissory Note Template California - It might stipulate the maximum loan amount a borrower can receive based on criteria.

The application process for prospective students can be streamlined by utilizing the AZ Forms Online, which provides essential information and guidance on completing the Arizona University Application form correctly, thereby enhancing the chances of securing a spot at Arizona State University, Northern Arizona University, or the University of Arizona.

Loan Agreement Template Georgia - It can include provisions about loan transfers or assignment.

Filling out the New York Loan Agreement form is a straightforward process that ensures both parties understand their obligations. Completing this form accurately is essential for a smooth transaction. Follow these steps to ensure you fill it out correctly.

Once you have completed these steps, review the form carefully to ensure all information is accurate. Both parties should retain a copy for their records. This will help in maintaining transparency and accountability throughout the loan period.

Filling out and using the New York Loan Agreement form requires careful attention to detail. Here are some key takeaways to consider:

By keeping these points in mind, you can navigate the process of completing and utilizing the New York Loan Agreement form with confidence.

Filling out a New York Loan Agreement form can seem straightforward, but many individuals make common mistakes that can lead to complications later on. Understanding these pitfalls can help ensure a smoother process. One frequent error is failing to provide accurate personal information. This includes not only names but also addresses and contact details. Inaccuracies can cause delays and misunderstandings between parties involved.

Another mistake often made is neglecting to read the terms and conditions thoroughly. Borrowers sometimes sign without fully understanding their obligations, which can lead to unexpected consequences. It's crucial to take the time to comprehend what is being agreed to, especially regarding interest rates and repayment schedules.

People also frequently overlook the importance of specifying the loan amount clearly. Ambiguities can create confusion and disputes later. It's essential to write the exact figure and ensure it matches any verbal agreements made prior to filling out the form.

Additionally, many individuals forget to include the purpose of the loan. This detail can be vital for both the lender and borrower. Clearly stating the purpose can help in case any questions arise during the loan period.

Another common error is not providing the necessary supporting documentation. Lenders often require proof of income, credit history, or other financial documents. Failing to include these can lead to delays in processing the loan.

Some borrowers mistakenly skip the signature section or forget to date the form. This oversight can render the agreement invalid. Always double-check to ensure that all required signatures are present and that the date reflects when the agreement was completed.

Moreover, individuals sometimes fail to keep copies of the completed loan agreement. Having a personal copy is essential for future reference. It can serve as a reminder of the terms agreed upon and provide documentation in case of disputes.

Lastly, many people do not consult with a legal expert or financial advisor before signing the agreement. Seeking professional advice can help clarify any uncertainties and ensure that all aspects of the agreement are fair and understood. Taking these steps can significantly reduce the likelihood of making mistakes on the New York Loan Agreement form.

When entering into a loan agreement in New York, several other documents often accompany the main loan agreement to ensure clarity and legal protection for all parties involved. Understanding these forms can help you navigate the borrowing process more effectively. Here’s a brief overview of some key documents commonly used alongside a New York Loan Agreement.

Being aware of these documents and their purposes can significantly impact your borrowing experience. Each plays a vital role in defining the terms of the loan and protecting the interests of both parties. Always consider seeking professional advice to ensure all documents are in order and aligned with your financial goals.