Official Ohio Promissory Note Document

Official Ohio Promissory Note Document

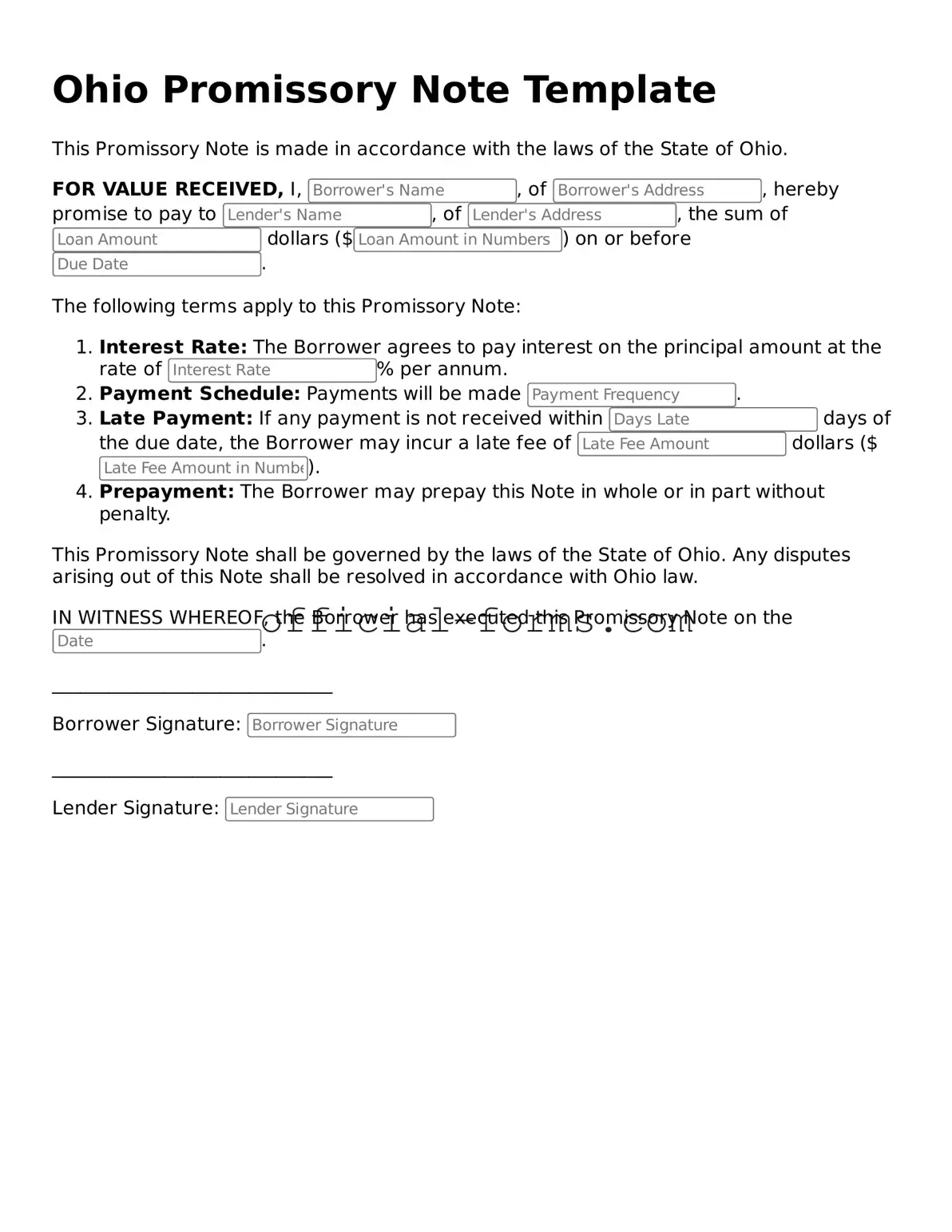

The Ohio Promissory Note form serves as a vital tool in financial transactions, allowing individuals and businesses to formalize a loan agreement. This document outlines the borrower's promise to repay a specific amount of money to the lender, detailing essential terms such as the loan amount, interest rate, repayment schedule, and any applicable late fees. By clearly stating these terms, the form helps to prevent misunderstandings between the parties involved. Additionally, it can include provisions for default, ensuring that both the lender and borrower understand the consequences of failing to meet the agreed-upon obligations. The Ohio Promissory Note is not only a legal document but also a safeguard for both parties, providing clarity and security in financial dealings. Understanding its components and implications is crucial for anyone considering entering into a loan agreement in Ohio.

How to Write a Promissory Note for a Personal Loan - It is common for the note to specify the governing law for potential disputes.

Promissory Note Template Illinois - It serves as a legal agreement between borrower and lender regarding payment obligations.

When engaging in a transaction involving a trailer in Georgia, the proper use of the Georgia Trailer Bill of Sale form is crucial for both parties involved. This document not only facilitates the verification of ownership but also simplifies the registration and titling process for the buyer. For more information, you can visit autobillofsaleform.com/trailer-bill-of-sale-form/georgia-trailer-bill-of-sale-form/.

Rhode Island Standard Promissory Note - Often seen as less formal than a loan agreement, a promissory note still holds significant legal weight.

Once you have the Ohio Promissory Note form in hand, it's time to fill it out accurately. This document will serve as a formal agreement between the lender and the borrower regarding the terms of a loan. Follow the steps below to ensure you complete the form correctly.

When dealing with the Ohio Promissory Note form, there are several important points to keep in mind. Understanding these can help ensure that the document serves its purpose effectively.

By following these key takeaways, both lenders and borrowers can navigate the Ohio Promissory Note form with confidence and clarity.

Filling out an Ohio Promissory Note form can seem straightforward, but many people make common mistakes that can lead to confusion or even legal issues down the line. Understanding these pitfalls can save you time and ensure your document is valid. Let's explore seven frequent errors that individuals encounter.

One of the most common mistakes is failing to include all necessary parties. A Promissory Note typically requires the names and addresses of both the borrower and the lender. Omitting this information can create ambiguity about who is responsible for repayment. Always double-check that you’ve included complete and accurate details for everyone involved.

Another frequent error is neglecting to specify the loan amount clearly. It's crucial to write the amount in both numerical and written form. For example, if you are borrowing $5,000, you should write "Five Thousand Dollars ($5,000)." This redundancy helps prevent misunderstandings regarding the amount borrowed.

Many people also overlook the importance of detailing the interest rate. This is a key component of any loan agreement. If you leave this blank or write it ambiguously, you may face disputes later. Clearly stating the interest rate ensures that both parties have the same expectations regarding repayment.

Additionally, the repayment terms must be articulated clearly. This includes specifying the due date, the frequency of payments, and the method of payment. Vague terms can lead to confusion and disagreements. Make sure to outline these details explicitly to avoid any future complications.

Another common mistake involves failing to date the document. A Promissory Note must be dated to establish when the agreement begins. Without a date, it can be challenging to determine the timeline for repayment, which could lead to misunderstandings or disputes.

People often forget to sign the document. While this may seem obvious, it’s a critical step. A Promissory Note is not legally binding unless it is signed by the borrower. Ensure that all necessary signatures are included before finalizing the document.

Lastly, many individuals do not keep a copy of the signed Promissory Note. After signing, it’s essential to retain a copy for your records. This serves as proof of the agreement and can be invaluable in the event of a dispute. Always make sure both parties have copies of the signed document.

By being aware of these common mistakes, you can navigate the process of filling out an Ohio Promissory Note more effectively. Attention to detail will help ensure that your agreement is clear, binding, and free from misunderstandings.

When dealing with a promissory note in Ohio, several other forms and documents may accompany it to ensure clarity and legal compliance. Each document serves a unique purpose in the lending process, providing additional layers of protection for both the lender and the borrower. Understanding these documents can help you navigate the lending landscape more effectively.

Being aware of these documents can empower both borrowers and lenders. They play a crucial role in protecting interests and ensuring that all parties understand their rights and responsibilities. Always consider consulting with a legal professional to ensure that all documents are properly prepared and executed.