Attorney-Verified Single-Member Operating Agreement Template

Attorney-Verified Single-Member Operating Agreement Template

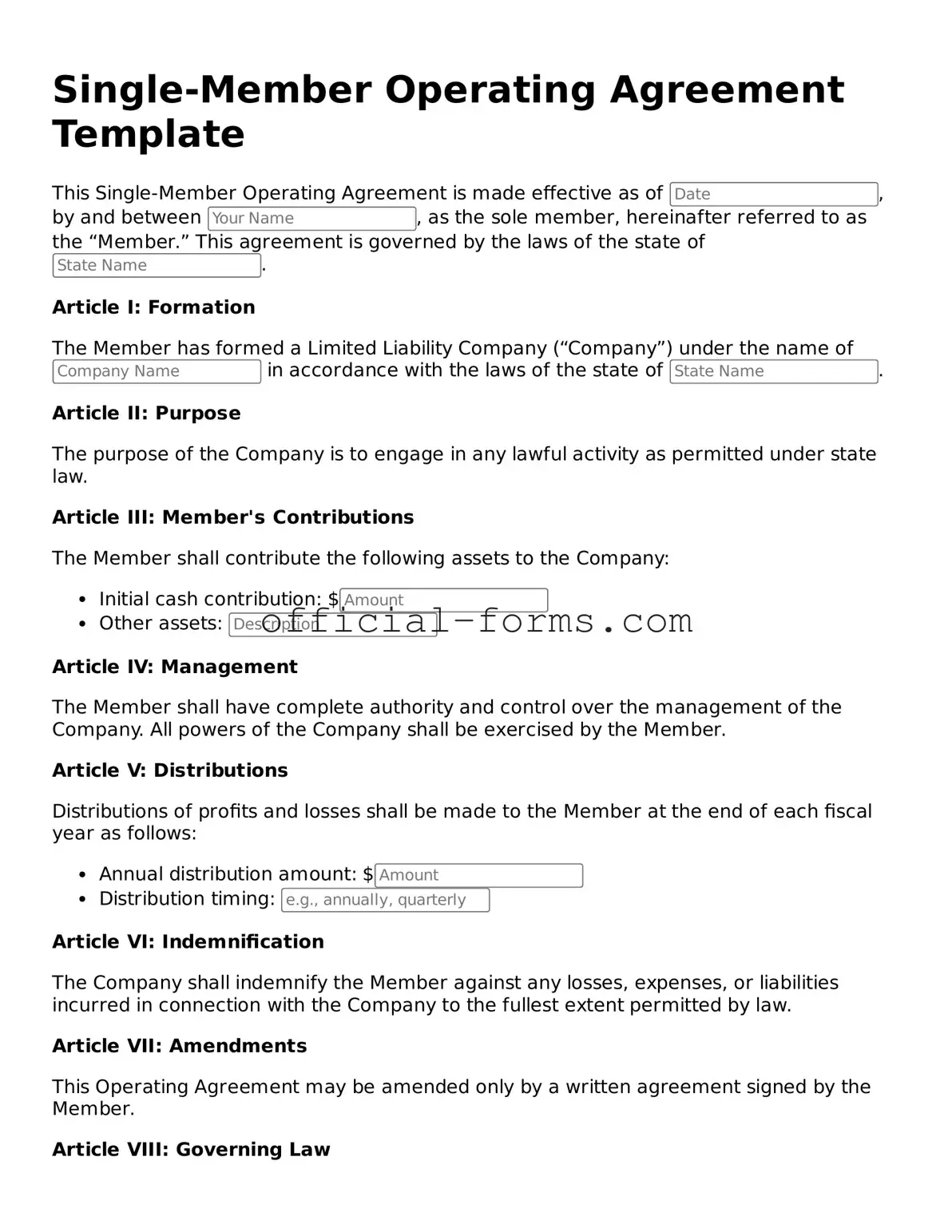

When starting a single-member limited liability company (LLC), having a clear and structured plan is essential for success. One important tool for this is the Single-Member Operating Agreement form. This document outlines the management structure and operational guidelines of the LLC, ensuring that the owner's intentions are clearly stated. It typically includes details about the ownership interest, decision-making processes, and how profits and losses will be handled. Additionally, the agreement can specify how the business will be managed, outline procedures for adding or removing members, and address what happens if the owner decides to sell the business or pass it on. By establishing these terms, the Single-Member Operating Agreement helps protect the owner's personal assets and provides a framework for the business's future. This form is not just a formality; it is a vital part of maintaining the LLC's legal protections and operational clarity.

After obtaining the Single-Member Operating Agreement form, you will need to provide specific information about your business. This document is essential for outlining the management structure and operational guidelines of your single-member entity. Follow the steps below to complete the form accurately.

Filling out and using a Single-Member Operating Agreement form is an important step for anyone operating a single-member LLC. Here are some key takeaways to keep in mind:

By keeping these takeaways in mind, you can ensure that your Single-Member Operating Agreement serves its intended purpose effectively.

Filling out a Single-Member Operating Agreement can be a straightforward process, but many individuals make common mistakes that can lead to complications down the line. One frequent error is failing to include essential information about the business. This includes the name of the LLC, the business address, and the purpose of the business. Without this information, the agreement may lack clarity and could create confusion regarding the entity’s operations.

Another mistake is neglecting to specify the ownership structure. Even though it’s a single-member LLC, it’s important to clearly state that the individual is the sole owner. This helps to reinforce the separation between personal and business assets, which is crucial for liability protection.

People often overlook the importance of defining the management structure. While a single-member LLC may seem straightforward, detailing how decisions will be made can prevent disputes later. For instance, specifying whether the owner will manage the business directly or appoint someone else can clarify expectations and responsibilities.

Additionally, many individuals forget to include provisions for handling changes in ownership or management. Life circumstances can change, and having a plan in place for transferring ownership or designating a successor can save time and legal trouble in the future.

Another common pitfall is not addressing the financial arrangements. It’s essential to outline how profits and losses will be distributed. This clarity ensures that the owner understands the financial implications of their decisions and can manage their tax obligations effectively.

Some people also fail to review the agreement thoroughly before signing. Rushing through the process can lead to mistakes or omissions that may have been easily corrected. Taking the time to read the document carefully can prevent misunderstandings and future legal issues.

Moreover, individuals sometimes neglect to date the agreement. A missing date can create ambiguity about when the terms were agreed upon. This might become problematic if any disputes arise, as the timeline of events can be crucial in legal matters.

Another mistake is not keeping a copy of the signed agreement. After completing the form, it’s important to store it in a safe place. This ensures that the owner has access to the document when needed, especially during tax preparation or if legal questions arise.

Finally, many individuals fail to seek professional advice when necessary. While it’s possible to fill out the form independently, consulting with a legal or financial professional can provide valuable insights. This step can help ensure that the agreement meets all legal requirements and effectively protects the owner’s interests.

A Single-Member Operating Agreement is a crucial document for individuals who own a limited liability company (LLC) on their own. While this agreement outlines the management structure and operational procedures of the LLC, several other forms and documents often accompany it to ensure comprehensive legal compliance and clarity. Below are some of the key documents that may be used in conjunction with the Single-Member Operating Agreement.

Each of these documents plays a significant role in the establishment and operation of a single-member LLC. Together, they create a framework that helps protect the owner’s personal assets, ensures compliance with state laws, and facilitates effective business management. Understanding these documents is essential for anyone looking to navigate the complexities of business ownership.