Official Texas Promissory Note Document

Official Texas Promissory Note Document

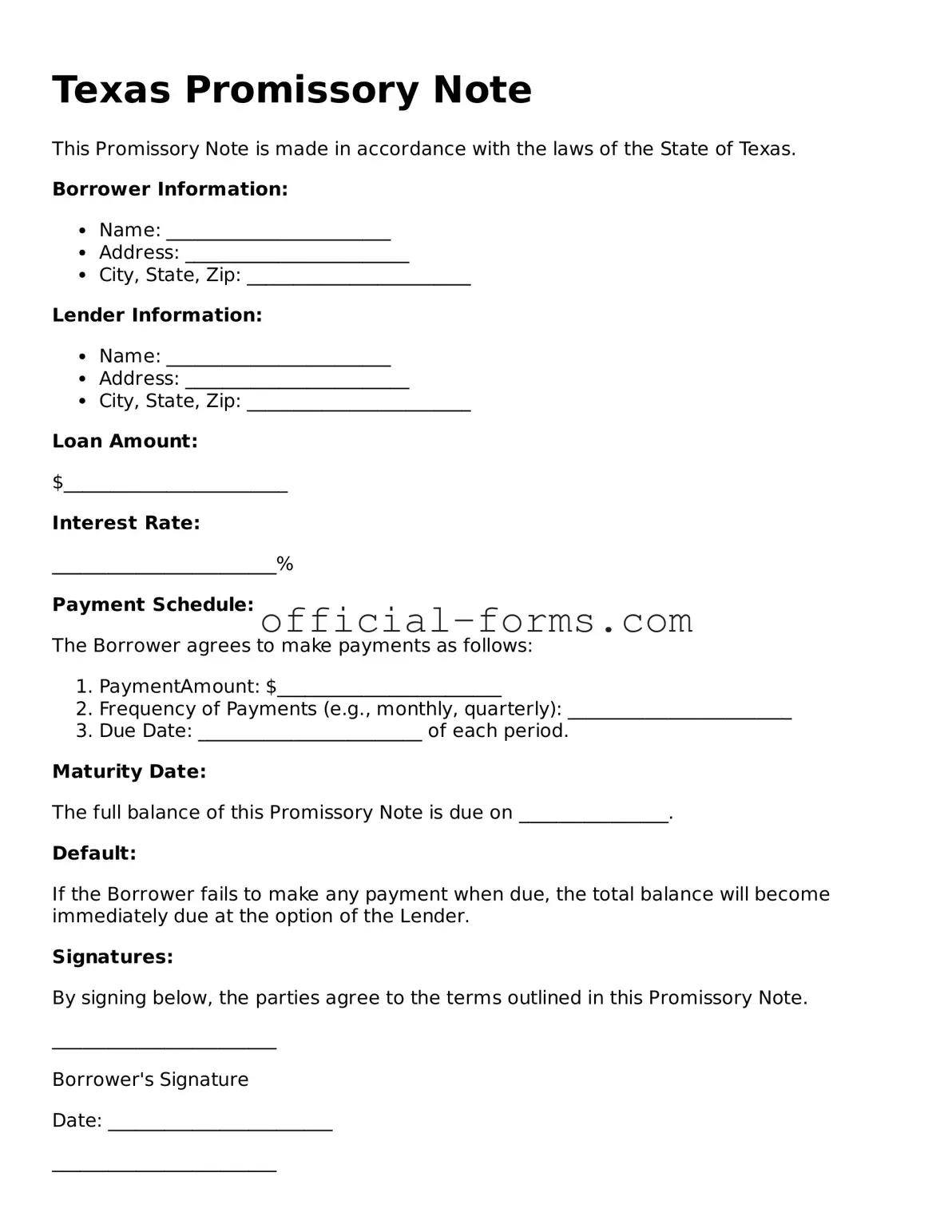

The Texas Promissory Note form serves as a crucial document in various financial transactions, providing a clear agreement between a borrower and a lender. This form outlines the amount borrowed, the interest rate, and the repayment schedule, ensuring both parties understand their obligations. It typically includes essential details such as the names of the involved parties, the date of the agreement, and any collateral securing the loan. Additionally, the Texas Promissory Note may specify the consequences of default, offering protections for lenders while clarifying the borrower's responsibilities. Understanding this form is vital for anyone engaging in lending or borrowing money in Texas, as it establishes the legal framework for the transaction and helps prevent disputes down the line.

How to Write a Promissory Note - It can include terms for late fees if the borrower misses a payment.

Ohio Promissory Note Requirements - This document outlines the terms of a loan agreement between a borrower and a lender.

Loan Note Template - It serves as a legal instrument that confirms the borrower's commitment to repay borrowed funds.

For individuals looking to facilitate a transfer of ownership, understanding the importance of a proper document is crucial. A well-prepared form, such as a thorough Mobile Home Bill of Sale, ensures that all necessary details are captured, benefiting both the buyer and seller in this legal process.

Promissory Note Template Illinois - Each party should receive a signed copy of the Promissory Note for their records.

After obtaining the Texas Promissory Note form, the next step involves accurately filling it out to ensure all necessary information is provided. This process requires attention to detail and clarity to avoid any potential issues in the future.

Once the form is filled out completely and accurately, it should be reviewed for any errors. After confirming all information is correct, copies can be made for both parties to retain for their records.

Understanding the Texas Promissory Note form is crucial for anyone involved in lending or borrowing money. Here are ten key takeaways to consider when filling out and using this form:

By adhering to these key points, individuals can navigate the complexities of the Texas Promissory Note form with greater confidence and clarity.

When filling out the Texas Promissory Note form, many people make common mistakes that can lead to confusion or legal issues. One frequent error is failing to include all necessary parties. It's essential to clearly identify the borrower and lender. Omitting a party can create complications later on.

Another mistake is not specifying the loan amount. The amount should be clearly stated in both numerical and written form. This helps prevent misunderstandings about how much is owed. If this step is overlooked, it can lead to disputes down the line.

Many individuals also neglect to include the interest rate. The interest rate should be clearly defined. Without it, the note may be considered incomplete, and the terms of repayment could become unclear.

Another common error involves the repayment schedule. Some people forget to outline when payments are due. A clear schedule helps both parties understand their obligations and avoid missed payments.

People often make mistakes with signatures. All required signatures must be present and legible. A missing signature can invalidate the note, so it's crucial to double-check this detail.

In some cases, individuals do not date the document. A date is important for establishing when the agreement was made. Without a date, it can be difficult to determine the timeline of the loan.

Another oversight is failing to include a default clause. This clause outlines what happens if the borrower fails to make payments. Not having this clause can leave both parties unprotected in the event of a default.

Some people also overlook the importance of notarization. While not always required, having the document notarized can provide an extra layer of security. It helps verify the identities of the parties involved.

Lastly, individuals may forget to keep copies of the signed document. Both parties should retain a copy for their records. This ensures that everyone has access to the terms of the agreement if questions arise in the future.

When dealing with a Texas Promissory Note, several additional forms and documents may be required to ensure clarity and legal compliance. Each of these documents serves a specific purpose in the lending process, providing protection and outlining responsibilities for both the lender and borrower.

Understanding these additional forms and documents can help both lenders and borrowers navigate the complexities of financial agreements. Proper documentation fosters trust and clarity, ensuring that all parties are aware of their rights and responsibilities.