Official Virginia Promissory Note Document

Official Virginia Promissory Note Document

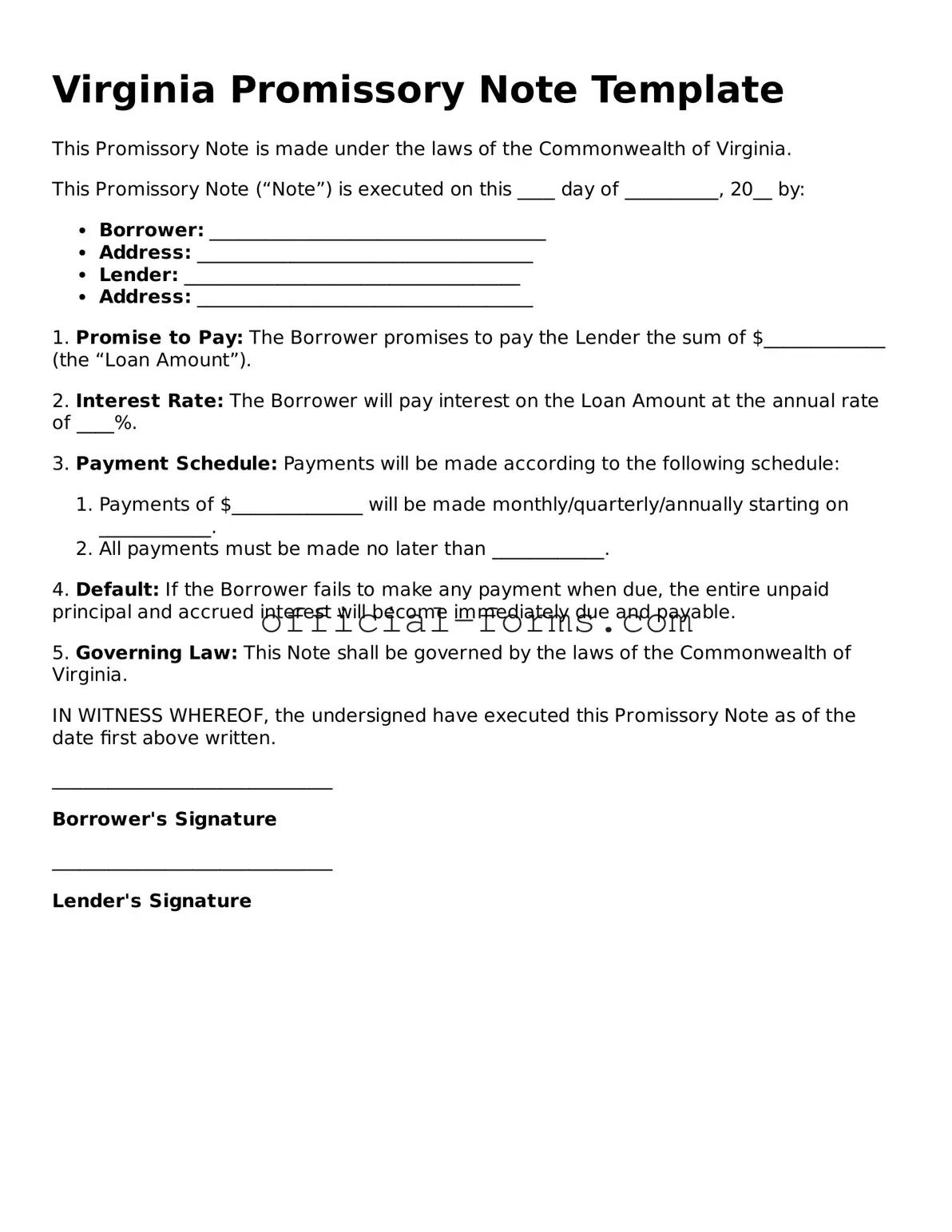

The Virginia Promissory Note form serves as a crucial financial document that outlines the terms of a loan between a borrower and a lender. This form typically includes essential details such as the principal amount borrowed, the interest rate, and the repayment schedule, ensuring that both parties have a clear understanding of their obligations. Additionally, it often specifies the consequences of default, providing a safety net for the lender while also informing the borrower of potential repercussions. The form may also include provisions for prepayment, allowing borrowers the flexibility to pay off the loan early without incurring penalties. By utilizing this standardized document, individuals and businesses in Virginia can facilitate secure lending transactions while minimizing misunderstandings and disputes. Overall, the Virginia Promissory Note is an important tool that fosters trust and transparency in financial agreements.

Promissory Note Georgia - Simplified notes may not require extensive documentation beyond basic terms, while more complex loans may necessitate additional details.

When engaging in the sale or purchase of a trailer in Florida, it is essential to utilize the Florida Trailer Bill of Sale form, which can be found at https://autobillofsaleform.com/trailer-bill-of-sale-form/florida-trailer-bill-of-sale-form/. This document serves as a crucial record for both the seller and the buyer, providing necessary legal protections and detailing the specifics of the transaction, thus facilitating a smooth registration process.

Utah Promissory Note - It may also specify whether payments are due monthly, quarterly, or annually.

Once you have the Virginia Promissory Note form in hand, you can proceed to fill it out. This document will require specific information about the loan agreement between the borrower and the lender. Make sure to have all relevant details ready before you start.

When filling out and using the Virginia Promissory Note form, keep these key takeaways in mind:

Filling out a Virginia Promissory Note form can be a straightforward process, but many individuals make common mistakes that can lead to complications. One frequent error is failing to include the correct date. The date signifies when the agreement takes effect, and omitting it can create confusion about the timeline of the loan.

Another common mistake is not providing accurate names and addresses for all parties involved. It is essential to clearly identify both the borrower and the lender. Incomplete or incorrect information can lead to disputes later on, complicating the enforcement of the note.

People often overlook the importance of specifying the loan amount. While it may seem obvious, a missing or incorrect figure can lead to misunderstandings. Clarity in this area is crucial to ensure that both parties have the same expectations regarding repayment.

Additionally, individuals sometimes forget to outline the terms of repayment. This includes the frequency of payments, the due date, and any applicable interest rates. Without clear terms, the borrower may find themselves confused about when and how much to pay, leading to potential default.

Another mistake is neglecting to include any late fees or penalties. If the borrower fails to make a payment on time, the lender should have a clear understanding of the consequences. Failing to specify these terms can lead to disputes and frustration.

Some individuals also make the error of not having the document signed by both parties. A promissory note is only enforceable if both the borrower and lender agree to its terms. Ensure that signatures are present to validate the agreement.

People may also forget to have the document witnessed or notarized, depending on their specific needs. While not always required, having a witness or notary can provide additional security and legitimacy to the agreement.

In some cases, individuals may fail to keep a copy of the signed note for their records. It is vital for both parties to retain a copy of the agreement. This can serve as a reference point in case any issues arise in the future.

Finally, a lack of attention to detail in reviewing the completed form can lead to errors. Before submitting the form, take the time to read through it carefully. This simple step can prevent many of the mistakes mentioned above, ensuring a smoother transaction.

When preparing a Virginia Promissory Note, there are several other forms and documents that are often used to complement it. These documents help clarify the terms of the agreement, protect the interests of the parties involved, and ensure that the transaction is legally sound. Below is a list of commonly associated documents.

Using these documents in conjunction with a Virginia Promissory Note can help create a clear and enforceable agreement. Each document plays a vital role in protecting the interests of both the lender and the borrower, ensuring a smooth transaction.